Apple & Google Blink on IAP Fees - AdTech Quietly Rewrites the Rules

IAP commission/fee war & Mobile AdTech Q4'25 round up (yes it's long overdue, but...I was...waiting for Mintegral earning report 🥺.

This one's going to be a bit long - so grab a coffee! ☕

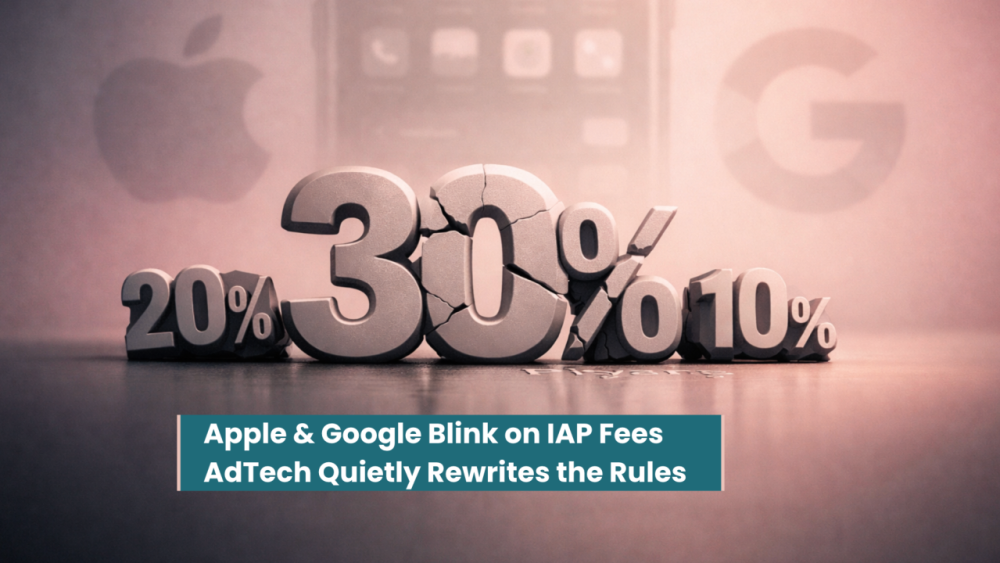

Apple & Google Finally Giving Devs a Break on IAP Fees

Back in my 2026 predictions, I called it: the big platforms would have to ease up on fees under pressure post Epic Games lawsuit. And yep, Google is blinking first, Apple easing in China, both (hopefully) are becoming way more dev-friendly than we've seen in years. 😏

Google's Big Move: A "New Era" for Android Billing

In their March 4, 2026 blog post (post-Epic settlement vibes), Google announced real choice and serious fee cuts:

- Billing flexibility: Devs can now use their own in-app billing alongside Google Play Billing, or even direct users to external websites for purchases.

- Registered App Stores program: Third-party app stores that register and meet safety/quality standards get smoother sideload experiences (fewer scary warnings).

- New fee structure (separating billing and service fees): Billing fee (if using Google Play Billing): Just 5% in EEA, UK, US (varies elsewhere). Service fee for IAP: New installs (post-rollout): 20% (down from 30%). Recurring subscriptions: Only 10%. Bonus tiers via Apps Experience Program or Google Play Games Level Up: Even lower (15% for new installs, 20% for existing).

Rollout timeline:

- Now through June 30, 2026: EEA, UK, US.

- By Sept 30, 2026: Australia.

- By Dec 31, 2026: Korea, Japan.

- By Sept 30, 2027: Rest of the world.

Google is playing offense here - giving devs more options to keep the ecosystem competitive and wrap up the Epic drama. Huge win for IAP/sub-heavy products.

Apple Backs Down in China

Under antitrust heat from Beijing, Apple quietly dropped fees starting March 15, 2026 (Mainland China only, iOS + iPadOS):

- Standard IAP & paid apps: Down from 30% to 25%.

- Small Business Program or mini-apps: Renewals after year 1 drop from 15% to 12%.

Clear move to avoid deeper probes in their #2 market. Fingers crossed this spreads elsewhere - let's see.

2025 Earnings Recap: Mobile AdTech (Finally Posting After Mobvista Dropped Numbers 😅)

Alright, onto Earning Calls:

Mintegral (via parent Mobvista, HK:1860)

Full-year 2025 revenue: $2.05B (+35.7% YoY). Mintegral core: $1.96B (+35.9% YoY)

80% from AI-powered smart bidding. Gaming still king at $1.46B (74.6%), but non-gaming (e-commerce, utilities, short drama) added $499M. Solid expansion story.

Unity (U) – Grow Solutions (Ads/Monetization)

- FY 2025 Grow: $1.23B

- Q4: $338M (+11% YoY) Third straight quarter of growth, powered by AI Vector.

Legacy IronSource dropped another $7M QoQ, expected to be <6% of total Unity revenue in Q1 2026. (Still calling this one of the worst M&A deals in mobile adtech history… except maybe for the Yahoo stuffs 😅)

Things are looking up for Grow in H2 2025 - here's to a stronger 2026, Unity!

AppLovin (APP)

- Q4 revenue: ~$1.7B (+66% YoY)

- Full-year 2025: $5.48B (+70% from 2024).

Standout: Adjusted EBITDA margin at 84% - BEST in the business, and trading at the highest multiples (P/S >20x 🤤).

AXON 2 AI is the engine of growth, not to mention that AppLovin is aggressively pushing into e-commerce. Very interesting stuffs playing out in 2026.

Google / Alphabet (GOOGL)

Q4 ad revenue: $82.3B 🤑

- Search + other: $63.1B (+17%)

- YouTube: $11.4B (+9%)

- Network (AdMob, Ad Manager, etc.): $7.8B (-1.6%) Network has been in steady decline for quarters now - classic case of size not guaranteeing wins.

Meta (META)

Q4 ad revenue: $58.1B (+24% YoY). No separate Network (FAN/MAN) breakout anymore, but they're loudly signaling a return into gaming ads. (Worth watching.)

Bottom line in adtech right now: Being massive doesn't mean you win automatically (see: Google's Network slide). Real edge comes from focus + cutting-edge tech (especially AI). That's why the dark horses are pulling ahead.

You might also like

Home of the Gamesforum events series and leading mobile game analysis. Discover everything you need to know about mobile games marketing and monetization.